Pay at the pump

The figure above illustrates how a connected car pay at pump model could work:

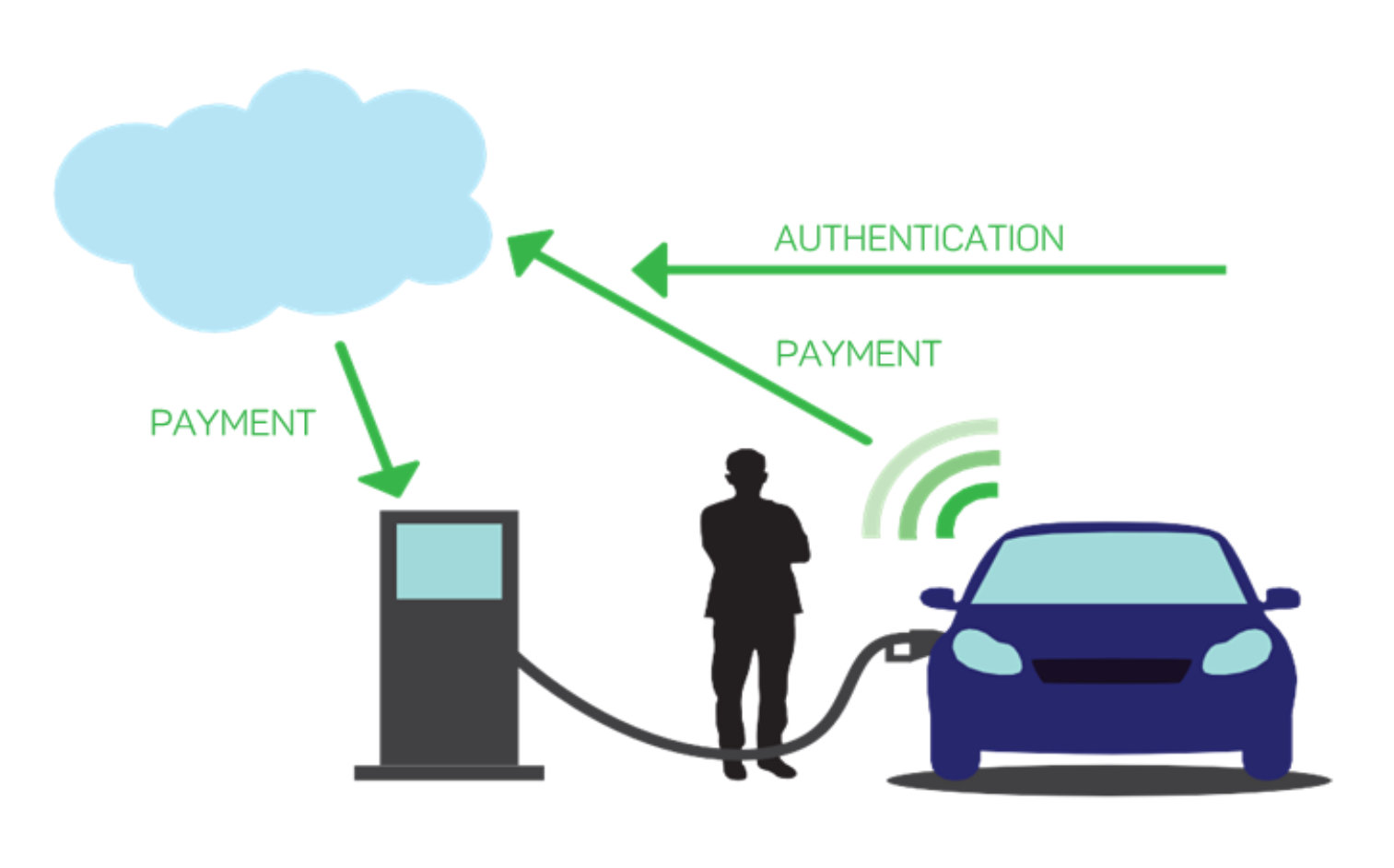

The figure above illustrates how a connected car pay at pump model could work:

- The driver fuels the car

- When triggered by the driver, the IVI system communicates with the pump, using a secure, short range wireless connection, providing authentication. This may happen whilst refueling is in progress

- When the driver has completed refueling and the authentication process, the car transfers money to the fuel company electronically, over the internet

Pump technology

For the connected car pay at pump use case we also need to consider the necessary changes to the fuel pump. It is already commonplace to allow a user to pay for their fuel at the pump, using a payment card. In this regard, the pump includes the hardware and software of standalone payment terminals. These terminals frequently include an embedded OS, such as Windows or Linux – this implies that the pump is designed in such a way to make software modification relatively simple. Generic payment terminals usually permit chip, magnetic strip and contactless modes of payment. Existing Pay at Pump solutions are mostly based on chip and PIN; some form of enhanced contactless payment must be added to the pump. As the payment terminals are based on embedded OSs, the necessary protocols and hardware abstractions are already available. The addition of hardware support for contactless payment is also similar to the IVI scenario.The future

All the necessary software and hardware components together with the processes for the creation of the connected car pay at pump use case are currently available. The creation of a commercially viable, fully integrated solution is the next step and there are no technical or regulatory barriers to doing so. While connected car payments is one example there are myriad other potential use cases including: road tolls, parking, car taxation, servicing, regulatory periodic vehicle testing, drive-thru restaurants, car rental, insurance and in-car entertainment. It is anticipated that the overlap of the automotive and fintech sectors will come to fruition in 2018, as IVI systems mature to provide a more generic (if not open) platform on which third-party developers can provide innovative new software and services. The IVI system is at the heart of the connected car; in the same way that the mobile market rapidly expanded as mobile platforms matured, so too will the connected car market. The majority of large businesses now have distinct digital and mobile strategies for selling and deploying their products and services. Within a few years, it is likely that many of these will also have a distinct connected car strategy. Such strategies will also include an element of monetization which requires integrated payment solutions. Will mobile payment technology spawn a platform to support connected cars — car payments? The rise of the fintech companies, challenger banks and changes to regulation of the financial services market in the EU have all stimulated significant innovation. In particular, the Payment Services Directive (PSD2) is allowing smaller financial organisations to provide services competitively. PSD2 is focused on electronic payments and will therefore extend the use of such payments further. PSD2 compels banks to allow 3rd parties to extend electronic payment options – for example to assign a payment card to the bank account or to initiate a money transfer from the account. The regulation changes are also allowing finance companies to sell each other’s products and services, broadening competition and creating niches in which the smaller fintech companies can innovate. This is changing the world of mobile payment technology. It is also likely to have the same impact on connected car payments. Further, the new fintech services being developed for deployment on mobile will also be deployed in an automotive context. In the embedded and automotive domains, the most significant opportunities for innovation in this area arise from the integration of IoT solutions. Sensors being added to cars and the smart cities in which they drive provide a plethora of potential new services, such as smart parking and insurance. These services will require seamless payment solutions as we increasingly expect to be able to make such payments, particularly from within our cars.Author – Jim Carroll, CTO, Mobica Courtesy of Mobile Payments Today