Fiat, Chevrolet and Volkswagen continue to lead the market and have increased their market share to represent 52% all together. Also worth mentioning is the dominant position of Fiat with 41% share of LCV. (67% for FCA, GM and VW on LCV).

Fiat, Chevrolet and Volkswagen continue to lead the market and have increased their market share to represent 52% all together. Also worth mentioning is the dominant position of Fiat with 41% share of LCV. (67% for FCA, GM and VW on LCV).

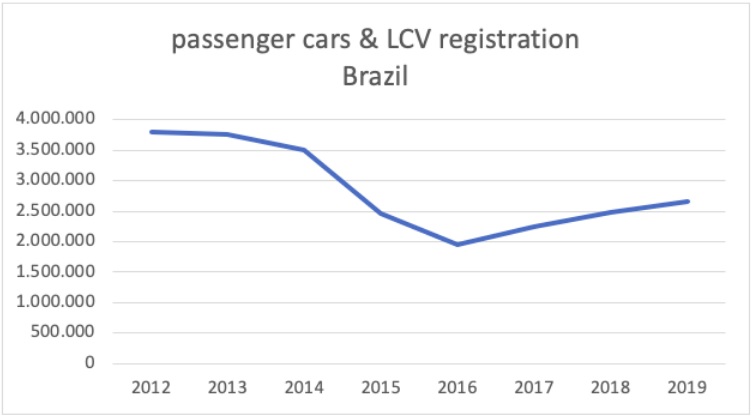

Passenger car and LCV registrations in Brazil

| 2018 | 2019 | Growth | |||

| Registration | Market Share | Registration | Market Share | ||

| FCA | 496,080 | 18.61% | 433,110 | 17.50% | 14.54% |

| GM | 475,747 | 17.85% | 434,420 | 17.55% | 9.51% |

| VW | 411,005 | 15.42% | 366,912 | 14.82% | 12.02% |

| Renault | 293,150 | 8.97% | 214,814 | 8.68% | 11.33% |

| Ford | 218,601 | 8.20% | 226,521 | 9.15% | -3.50% |

| Toyota | 216,899 | 8.14% | 200,920 | 8.12% | 7.95% |

| Hyundai | 193,956 | 7.28% | 186,655 | 7.54% | 3.91% |

| Honda | 129,130 | 4.84% | 131,601 | 5.32% | -1.88% |

| Nissan | 96,088 | 3.60% | 97,515 | 3.94% | -1.46% |

| PSA | 47,781 | 1.79% | 44,008 | 1.78% | 8.57% |

| Others | 141,146 | 5.30% | 138,873 | 5.61% | 1.64% |

| Total | 2,665,583 | 100.00% | 2,475,349 | 100.00% | 7.69% |

Leaseco portfolios

| 2018 | 2019 | Growth | |

| Unidas | 72,000 | 85,000 | 18.06% |

| Localiza | 48,056 | 67,589 | 40.65% |

| Movida | 37,000 | ||

| ALD | 26,300 | 32,000 | 21.67% |

| LM Frotas | 23,000 | ||

| Arval | 24,000 | 22,500 | -6.25% |

| Ouro Verde | 20,000 | 22,000 | 10.00% |

| LeasePlan | 10,230 | 13,300 | 30.35% |

| Lets | 6,500 | ||

| Rodobens | 3,000 | ||

| VWFS | 1,211 | 1,500 | 23.86% |

| Total | 218,770 | 313,389 | |

| Estimated market growth | 14.62% | ||

| New business 2019 | 167,542 |

- Local heroes like Localiza and Unidas are combining fleet management with daily rental success, focusing on local customers (comparable to the Sixt model in Germany)

- International lessors like ALD, Arval and LeasePlan concentrate on international customers and lease and fleet management only.